Mark Paccione discusses how current GDP forecasts may affect the U.S. economy and why we should remain optimistic about the future of investments.

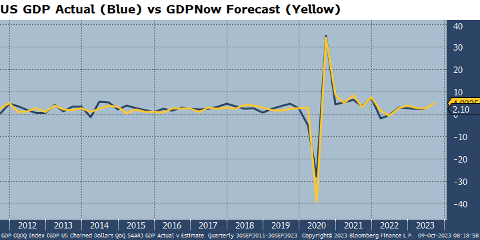

While the economy appears to be humming, there is popular sentiment to the contrary. The Atlanta Fed GDPNow, a real-time forecast of nominal U.S. GDP, is tracking at 4.9% as of September 30, 2023, up from the June 30 reading of 2.2%. While it’s only an estimate, the index does a reasonably good job of predicting actual GDP, as shown in the chart below:

Source: Bloomberg Finance, LP. October 9, 2023.

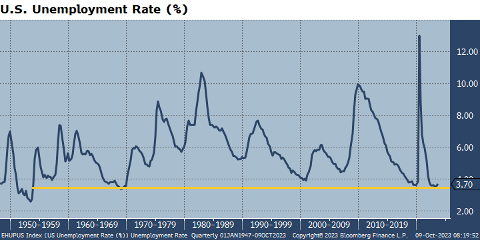

One reason the economy remains strong is the job market. While the unemployment rate has recently ticked higher to 3.8%, it remains at historically low levels not seen since the 1960’s, as displayed in the chart below. [1]

Source: Bloomberg Finance, LP. October 9, 2023.

Cause for Concern?

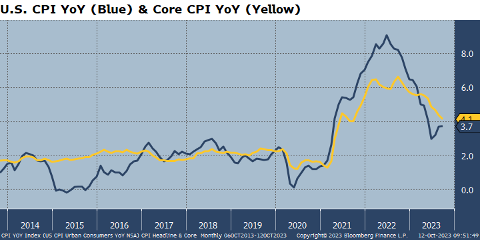

Given that GDP is above 4%, albeit in nominal terms, and unemployment is below 4%, you would think more people would be happy. Unfortunately, there are clouds on the horizon that have investors concerned. The primary focus of many investors remains inflation and interest rates. While inflation has come down, headline inflation (as measured by the Consumer Price Index) ticked higher recently, while core inflation, which strips out volatile food and energy, remains significantly higher than the Fed’s stated target of 2%.

Source: Bloomberg Finance, LP. October 12, 2023.

Considering the strong economy, tight labor market, and elevated inflation, it’s no wonder there’s concern that the U.S. Federal Reserve is not done raising rates. At the very least, it’s safe to assume that the Fed will not cut rates anytime soon, unless the economy meaningfully deteriorates.

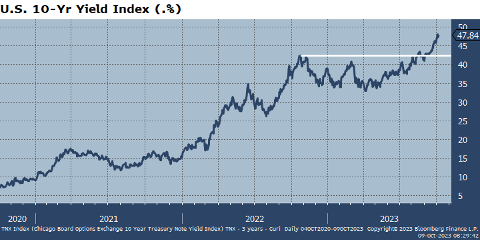

At the start of 2023, the market expected Fed rate cuts to begin sometime this year. Now, the first rate cut is expected in September 2024—and that’s only a 51% probability.[2] While savers are happy that they can now earn more than 5% on short-term treasurys, the most troubling market development is the recent, sharp rise in long-term interest rates. The 10-year U.S. Treasury yield made multi-year highs, closing the quarter at 4.6%, and is continuing even higher in October as it’s reached levels not seen since 2007.

Source: Bloomberg Finance, LP. October 9, 2023.

Remember, the 10-year U.S. Treasury yield nearly tripled from 1.5% on December 31, 2021, to 4.3% on October 22, 2022. The sharp rise in rates was the primary driver of the 2022 market sell-off that saw the S&P 500 down -18% and the Bloomberg Aggregate Bond Index down -13% for the year. Investors fear the recent breakout in long-term rates may result in another stock market drop, another bank failure, a sharp slowdown in housing and commercial real estate, and/or potentially tip the economy into recession.

The Glass is Half Full

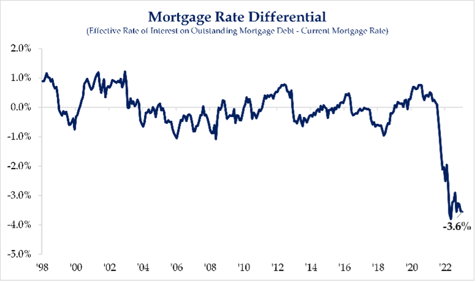

Despite these fears, there are reasons for optimism. By all accounts, the U.S. economy remains strong, consumer and corporate balance sheets remain healthy, artificial intelligence is expected to be a long-term productivity booster, and interest-rate sensitive sectors like housing held up remarkably well, considering the meteoric rise in rates last year. While higher lending rates do slow an economy, the increase in rates over the past year and a half has not been as much of a headwind as anticipated.

As succinctly stated by the experts at Strategas, “The current prevailing rate on 30-year fixed rate mortgages has certainly impaired housing activity given the low levels of existing home sales. However, it’s important to keep things in perspective given that the majority of outstanding mortgage debt in the U.S. has a fixed rate nearly -300 bps [-3%] below current rates.”

Source: Grabinski, Ryan. “Contextualizing Consumer Resiliency to Higher Rates.” Strategas. September 20, 2023.

As for portfolio positioning, we believe there are ample investment opportunities in the current market environment. With long-term interest rates rising, we continue to favor investments that pay significant yields with low interest rate risk. Short-term treasuries yielding over 5% remain particularly attractive given the meaningful yield, low interest rate sensitivity, and little to no credit risk. We also like non-traditional debt sectors like CLOs, Real Estate Debt, and direct lending, as traditional banks remain hampered by the same conditions that saw Silicon Valley Bank and Signature Bank taken over by the FDIC. These non-bank lending opportunties currently provide significant yields that have held up very well in the recent rate rise, and we believe they will continue to do so should rates continue to increase.

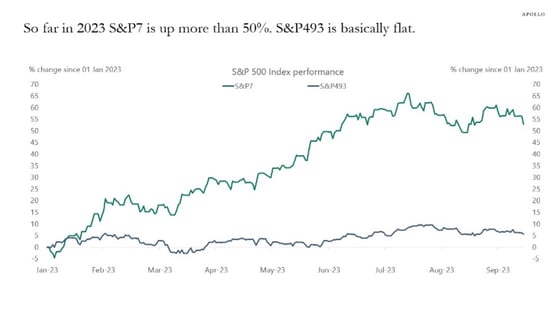

In stock markets, the S&P 500 and Nasdaq continue to lead year-to-date, as performance is dominated by a handful of large cap tech names, now referred to as the Magnificent Seven. These include: Microsoft, Meta, Amazon, Apple, Nvidia, Alphabet, and Tesla. While the Magnificient Seven have been propelled to lofty valuations by the hope and hype surrounding artificial intelligence (AI), many other stocks have traded sideways for the balance of the year. Small caps, mid caps, and international stocks trade at more attractive valuations than large growth stocks. Investors may be wise to rebalance their portfolios by trimming the more expensive parts of the stock market to add to parts that have lagged.

Source: Apollo Global Management. September 23, 2023.

As always, if you have any questions about your investment portfolio, want to see if you’re properly positioned for today’s current market environment, or are exploring what Curi Capital can do for you, please reach out to a member of our team at 984-202-2800.

Please note: This material should not be considered a recommendation to buy or sell securities or a guarantee of future results. Curi Wealth Management, LLC dba Curi Capital is a registered investment advisor. Registration does not imply a certain level of skill or training. More information about Curi Capital can be found in its Form ADV Part 2, which is available upon request.

Past performance is not a guarantee of future results. All investment strategies involve risk and have the potential for profit or loss; changes in investment strategies, contributions, or withdrawals may materially alter the performance and results of a portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client's investment portfolio. References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in an index and indexes do not reflect the deduction of the advisor's fees or other trading expenses.

Curi Capital clients should contact the Company if there have been changes in the client's financial situation or investment objectives, or if the client wishes to impose any reasonable restrictions on the management of the client's account or reasonably modify existing restrictions.

[1] Source: Bloomberg Finance, LP

[2] Source: WIRP, Bloomberg Finance, LP. September 30, 2023.

.png?width=352&name=MicrosoftTeams-image%20(30).png)

Comments